Getting hurt in a Philadelphia car crash is a chaotic experience; navigating Pennsylvania’s complex auto insurance system makes it even more overwhelming. Many drivers assume that if the other driver caused the crash, the at-fault driver’s insurance will automatically and immediately pay their hospital bills. In Pennsylvania, this is not how it works.

This guide breaks down exactly how Personal Injury Protection (PIP) works for Philadelphia drivers, ensuring you don’t make a costly mistake when the medical bills start piling up.

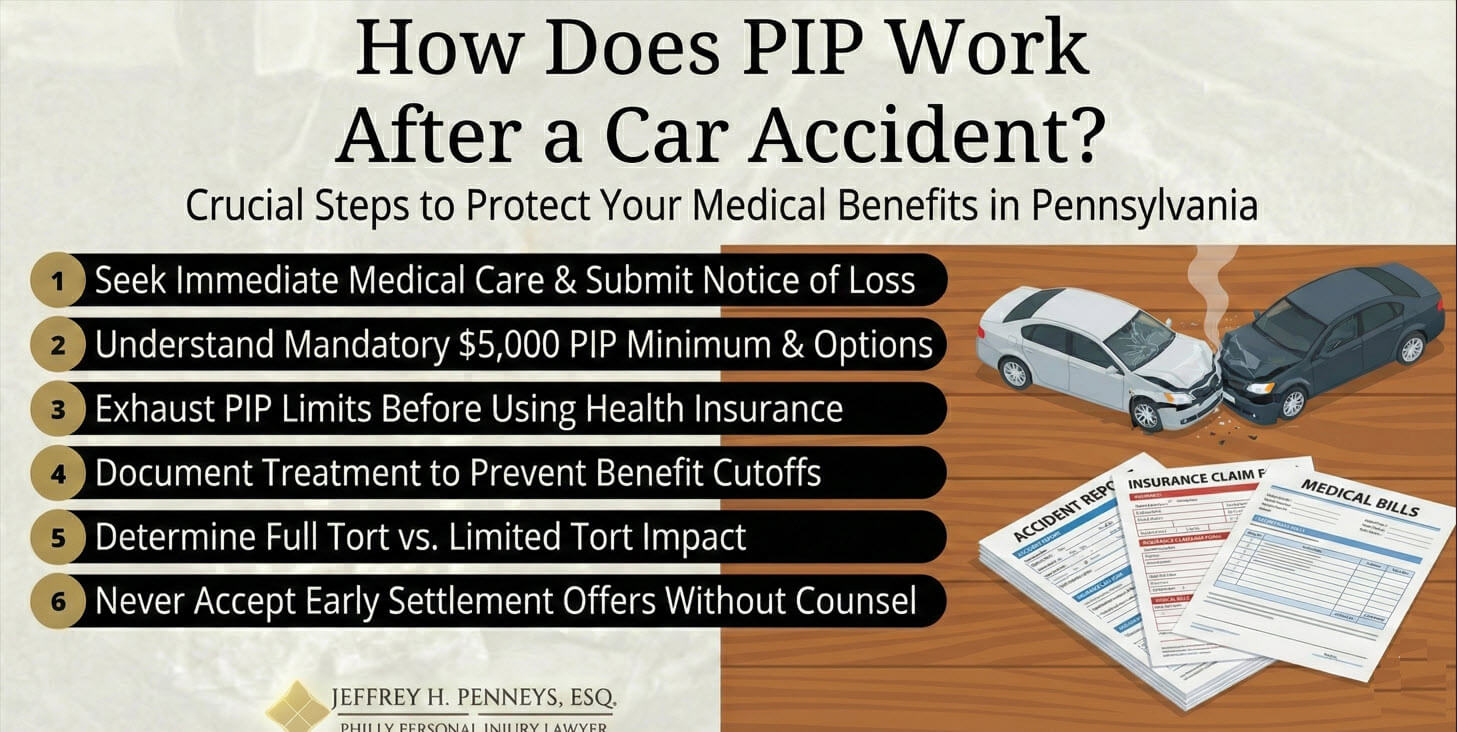

Securing Medical Treatment and Initiating Your PIP Claim

You must seek medical attention immediately to establish medical causation. Once treated, you are contractually obligated to provide a Notice of Loss to your insurance carrier. You must promptly submit an Application for Benefits to open your PIP claim. Failing to submit this paperwork within the required timeframe gives your insurance company leverage to delay or deny your medical coverage, leaving you personally responsible for the ER bills.

Understanding PIP Coverage Limits

Before a crash happens, you select your PIP limits on your auto insurance policy. The state of Pennsylvania requires all drivers to carry a mandatory minimum of $5,000 in Medical Benefits, but many drivers purchase higher limits or optional coverages to protect their assets.

The table below outlines how PIP protection is structured in Pennsylvania:

| Type of PIP Coverage | State Requirement | What It Covers in Pennsylvania |

| Medical Benefits | Mandatory (Minimum $5,000) | Covers necessary medical costs: ambulance rides, ER visits, surgeries, physical therapy, and necessary medical equipment. |

| Income Loss Benefit | Optional | Reimburses a percentage of your gross income (typically 80%) if your crash injuries prevent you from working. |

| Accidental Death Benefit | Optional | Provides a lump sum to your beneficiaries if the accident results in fatal injuries within 24 months. |

| Funeral Expense Benefit | Optional | Covers reasonable burial or cremation costs following a fatal motor vehicle accident. |

| Extraordinary Medical | Optional | Provides extended coverage (often up to $1 million) for catastrophic injuries requiring lifelong, specialized care. |

Coordinating your PIP Benefits

In Pennsylvania, PIP is the primary” payer for auto accident injuries. You must exhaust your PIP limits (e.g., your $5,000 minimum) before your private health insurance kicks in to cover the remaining medical bills

A common mistake injured drivers make is handing the hospital billing department their private health insurance card (like Blue Cross or Aetna) instead of their auto insurance information.

If you attempt to bypass your auto insurance, your health insurer will likely deny the claim once they discover the injuries stem from a motor vehicle accident, creating a billing headache that can send your accounts to collections.

Protecting Your Benefits from Insurance Tactics

Even though you are dealing with your own insurance company for PIP, it is still a for-profit business focused on its bottom line. If your treatment for soft-tissue injuries or whiplash lasts longer than their internal algorithms deem necessary, they may force you to attend an Independent Medical Examination (IME).

Despite the name, these doctors are paid by your insurance company. Their primary goal is often to declare that you have reached Maximum Medical Improvement (MMI) so the insurer can legally cut off your PIP benefits. You must have a paper trail of consistent, documented medical treatment to fight back against premature PIP terminations.

Executing Third-Party Liability Claims

Your PIP coverage pays strictly for your economic damages (medical bills and, if selected, lost wages). It does not pay for your physical pain, mental anguish, or loss of life enjoyment. To recover these damages, you must pursue a Third-Party Liability Claim against the at-fault driver.

Your ability to do this hinges on the tort option you selected on your policy:

- Full Tort: You retain the unrestricted right to sue the at-fault driver for all non-economic damages (pain and suffering), regardless of the severity of your injury.

- Limited Tort: If you selected Limited Tort to save money on your premium, you forfeit your right to sue for pain and suffering unless your injuries meet Pennsylvania’s strict definition of a “serious injury” (such as permanent disfigurement or severe impairment of a body function).

Never accept an early settlement release from the at-fault driver’s insurance without a legal review, as this permanently waives your right to future compensation once your PIP runs out.

Answers to Your Pennsylvania PIP Questions

Will my insurance rates increase if I use my PIP benefits for a crash I didn’t cause?

Under Pennsylvania law, insurers are generally prohibited from raising your premium or adding a surcharge simply because you filed a PIP medical claim for an accident where you were not at fault.

Does PIP cover the damage to my vehicle?

No. PIP strictly covers bodily injuries and related economic losses. Vehicle repairs are covered by your Collision coverage or the at-fault driver’s Property Damage Liability coverage.

What happens when my medical bills exceed my $5,000 PIP limit?

Once your PIP is exhausted, your private health insurance becomes the secondary payer. If you are left with co-pays, deductibles, or excess bills, you will then seek compensation for those out-of-pocket costs through a claim against the at-fault driver.

Do I have to see a specific “network” doctor under PIP?

No. You have the right to choose your own medical providers. Your auto insurance company cannot dictate which doctor, chiropractor, or physical therapist you see for your accident-related injuries.

Can PIP cover me if I was hit by a car as a pedestrian?

Yes. If you are struck by a motor vehicle while walking or cycling in Philadelphia, your own auto insurance policy’s PIP coverage will act as the primary payer for your medical treatment.

If I was a passenger in my friend’s car, whose PIP applies?

If you have your own auto insurance policy (or live with a relative who does), your own PIP applies first. If you do not have auto insurance in your household, you would typically use the PIP coverage of the vehicle you were riding in.

Should I delay medical treatment if my injuries feel minor?

Absolutely not. Delaying treatment creates a “gap in care,” giving your insurance company a valid excuse to argue your injuries were not caused by the crash, which frequently results in a denied PIP claim.

Can I cash out my unused PIP benefits?

No. PIP is a use-it-or-lose-it medical benefit. It only pays directly to your medical providers for actual, verified treatment rendered. You cannot receive a check for the balance of your unused limits.

Will my health insurance demand to be paid back if I win a lawsuit?

Often, yes. This is known as a subrogation lien. If your health insurance pays for surgeries or rehab after your PIP runs out, they have a legal right to recover what they spent directly from your final personal injury settlement.

Why is the other driver’s insurance asking me for a recorded statement?

They are actively looking for you to say something that minimizes your injuries or admits partial fault (even 1%). Do not give a recorded statement to the at-fault driver’s insurance adjuster without first speaking to an attorney.

Call Jeffrey Penneys for 30 Years of Experience Winning Car Accident Claims

Navigating PIP applications, independent medical exams, health insurance subrogation, and limited tort thresholds requires an aggressive legal strategy. Insurance adjusters are heavily trained to minimize your payouts, leaving you to deal with the medical debt.

Call Philly Personal Injury Lawyer Jeff Penneys today at (215) 771-0430 or book online for a free car accident consultation. Let Jeff handle the insurance companies and protect your rights so you can focus on healing.